Emirates NBD (DFM: EmiratesNBD), a leading bank in the region, delivered a solid set of results with net profit up 4% y-o-y and 1% q-o-q to AED 1.87 billion. The operating performance was helped by a control on expenses and lower provisions.

Net profit up 4% y-o-y and 1% q-o-q to AED 1.87 billion

Dubai, 19 April 2017

Emirates NBD (DFM: EmiratesNBD), a leading bank in the region, delivered a solid set of results with net profit up 4% y-o-y and 1% q-o-q to AED 1.87 billion. The operating performance was helped by a control on expenses and lower provisions. Net interest income improved 1% q-o-q due to loan growth coupled with an improvement in margins. Core gross fee income increased 27% q-o-q and 7% y-o-y on the back of higher income from forex and rates. Net interest margin improved during the quarter as rate rises flowed into loan yields and funding pressures receded. The Bank’s balance sheet continues to strengthen with further improvements in credit quality and liquidity, coupled with solid capital ratios.

Financial Highlights – Q1 2017

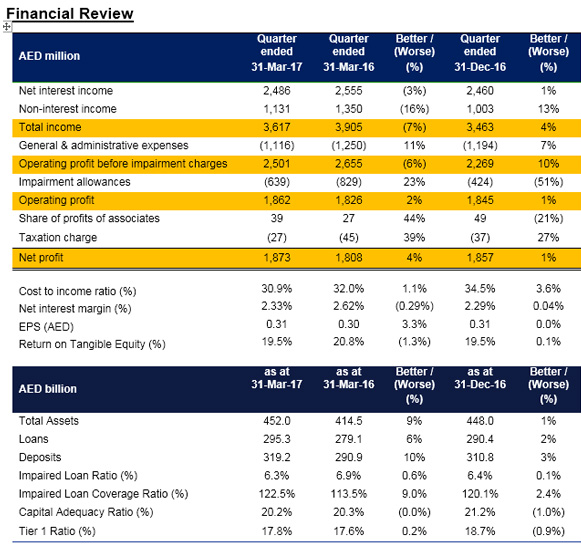

- Net profit of AED 1.87 billion, up 1% q-o-q and 4% y-o-y

- Total Income of AED 3.6 billion, up 4% q-o-q and declined 7% y-o-y due to lower gains from the sale of investments

- Total assets at AED 452.0 billion, up 1% from end 2016

- Customer loans at AED 295.3 billion, up 2% from end 2016

- Customer deposits at AED 319.2 billion, up 3% from end 2016

- Net Interest Income improved 1% q-o-q on loan growth coupled with an improvement in margins

- Core gross fee income increased 27% q-o-q on the back of higher income from forex and rates

- Cost of risk improved to 80 basis points as an impairment charge of AED 639 million is 23% lower than in Q1-16, helped by AED 364 million of writebacks and recoveries

- Impaired Loan ratio improved to 6.3% whilst the Impaired Loan Coverage ratio strengthened to 122.5%.

- Advances to Deposit ratio at 92.5% remains comfortably within the management’s target range

- Tier 1 Capital Ratio declined to 17.8% as retained profit was more than offset by the payment of the annual dividend

Commenting on the Group’s performance, Mr. Hesham Abdulla Al Qassim, Vice Chairman and Managing Director, Emirates NBD said: “Emirates NBD made an encouraging start to the year with a 4% growth in net profit and further strengthened its balance sheet, with improvements in credit quality and liquidity, coupled with strong capital ratios. We are delighted that our Investment Bank and Asset Management units successfully completed the UAE’s first IPO of 2017 with the launch of ENBD REIT. We are also particularly pleased to be ranked the UAE’s most valuable banking brand, and 75th worldwide, by The Banker. We are honoured to be part of the Year of Giving, an initiative launched by HH Sheikh Khalifa Bin Zayed Al Nahyan, the President of the UAE, to dedicate all activities during 2017 to the brave UAE martyrs; Emirates NBD has embraced the key concept of ‘giving’ as defined by HH Sheikh Mohammed bin Rashid Al Maktoum, Vice President & Prime Minister of the UAE and Ruler of Dubai, by ensuring that all our 2017 CSR activities are designed to make a difference to individuals, society and the nation as a whole.”

Group Chief Executive Officer, Shayne Nelson said: “Emirates NBD delivered a solid set of results in the first quarter of 2017. Net profit increased by 4% to AED 1,873 million, underpinned by a control on expenses and an improved cost of risk. The Group’s liquidity position remained strong and we are focused on improving margins by enhancing our funding base. We unveiled Liv., the UAE’s first digital bank targeted at millennials, which offers a differentiated digital experience for a new generation of customers. We are well positioned to utilise our strong franchise, digital capabilities and financial strength to take advantage of growth opportunities within the region.”

Group Chief Financial Officer, Surya Subramanian said: “The operating performance for the first quarter of 2017 was pleasing as we saw margins improve compared to Q4-16. This margin increase is due to an improvement in funding costs coupled with loan pricing benefiting from rising interest rates. I am also glad to see that the cost control measures implemented in 2016 have taken effect. The cost to income ratio, at 30.9%, is comfortably within management targets, enabling us to invest to support future growth. We also delivered a further improvement in credit quality and this, coupled with an improvement in margins, and lower costs is a position we expect to hold for the remainder of 2017.”

Total income for the quarter ended 31 March 2017 amounted to AED 3,617 million; an increase of 4% compared with AED 3,463 million in the preceding quarter.

Net interest income improved 1% over the preceding quarter due to loan growth coupled with an improvement in margins.

Core gross fee income increased 27% over the preceding quarter and 7% year-on-year on the back of higher income from forex and rates.

Costs for the quarter ended 31 March 2017 amounted to AED 1,116 million, an improvement of 11% over the previous year, helped by a reduction in staff costs following cost control measures implemented in 2016. Costs have now declined for 5 consecutive quarters. The cost to income ratio improved by 1.1% y-o-y to 30.9%, enabling us to invest to support future growth.

During the quarter, the Impaired Loan Ratio improved by 0.1% to 6.3%. The impairment charge in Q1-17 of AED 639 million is 23% lower than in Q1-16 as the net cost of risk improved. This net provision includes AED 364 million of write-backs and recoveries, and together helped boost the coverage ratio to 122.5%.

Net profit for the Group was AED 1,873 million in Q1-17, 4% above that posted in Q1-16. The increase in net profit was driven by asset growth, a control on expenses and reduced provisions which helped offset lower non-interest income.

Loans increased by 2% and Deposits grew by 3% during the quarter. The Advances to Deposits Ratio remains comfortably within Management’s target range at 92.5%. In Q1-17, the Bank raised AED 3.3 billion of term funding through private placements and term funding represents 10% of total liabilities.

As at 31 March 2017, the Bank’s capital adequacy ratio and Tier 1 capital ratio were 20.2% and 17.8% respectively.

Business Performance

Retail Banking & Wealth Management (RBWM)

RBWM delivered strong financial results in Q1 2017 with total income of AED 1,670 million, up 10% y-o-y, led by growth in net interest income from liabilities. Fee income grew 5% y-o-y and now comprises 37% of revenues.

RBWM’s liability book continued to grow faster than the market, increasing by AED 7.5 billion during Q1-17, led by growth in low cost Current Account and Savings Account (‘CASA’) balances. Total customer advances rose 2% over end 2016, from growth in mortgages.

The Personal Banking Beyond proposition for emerging affluent customers was re-launched offering enhanced benefits and features, with acquisition under this segment up 10% over the same period in 2016. Over 60% of new credit cards sourced belonged to the premium segment supported by acquisition campaigns for the Skywards and Starwood Preferred Guest co-brands.

The business continued to lead the digitisation and innovation space with the launch of EVA™ (Emirates NBD Virtual Assistant), the region’s first voice-based virtual chatbot powered by artificial intelligence. A paperless Personal Loan application programme was rolled out across branches providing easy and same day disbursement.

In February 2017, RBWM unveiled the UAE’s first digital bank targeted at millennials. Liv. is a mobile only proposition centered on lifestyle to provide a differentiated digital experience for young adults in managing their finances.

In line with the Bank’s commitment to support a low-carbon environment, the Green Auto Loan product was launched, offering customers discounted interest rates when purchasing electric or hybrid cars.

The bank was ranked as the UAE’s most valuable banking brand in The Banker’s annual brand valuation, as well as recognized as the Best Retail Bank in the UAE for 2017 by The Asian Banker.

Private Banking attracted additional Assets under Management from all client segments and replaced extraordinary income in previous quarters with core revenue. Emirates NBD Asset Management successfully listed the ENBD REIT on Nasdaq Dubai, having raised more than USD 100 million new money. Emirates NBD Securities benefited as trading volumes in local and regional capital markets improved in the first quarter.

Wholesale Banking (WB)

Wholesale Banking delivered a strong performance in the first quarter of 2017 with net profit of AED 763 million, up 8% over the corresponding period in 2016, arising from a combination of asset growth and margin improvement.

Net interest income of AED 824 million for the first quarter of 2017 was 6% higher than the same period in 2016 on the back of continued growth in lending.

Fee income of AED 318 million for the first quarter of 2017 improved over the corresponding period in 2016, reflecting continuing efforts to grow non-funded income with a strategic focus on growing the Bank’s cash management and trade finance business while Treasury and Investment Banking products, in particular, also showed good growth compared to 2016.

Costs were 4% lower for the period compared with the first quarter 2016, reflecting a conscious effort to drive efficiencies within the business. Wholesale Banking is upgrading its Transaction Banking systems and channels to digitise and further improve the levels of straight through processing. System upgrades in Global Markets & Treasury are enhancing product capabilities.

Credit quality of the loan book improved due to the successful resolution of legacy portfolio issues. This resulted in an improvement in coverage and a decline in provisioning requirements for the period.

Assets grew by 2% over the corresponding period in 2016, supported by good momentum in lending activity and a growth in the Bank’s Trade Finance business. Deposits fell by 5% reflecting efforts to optimise both the mix and cost of funding.

Wholesale Banking continues with its transformation programme to become the leading Wholesale Bank in the Middle East and North Africa. As part of the transformation, Wholesale Banking recently introduced industry specific customer segmentation to have a more focused approach to delivering a full range of Wholesale Banking products and solutions to the Bank’s customers across the Region.

Global Markets & Treasury (GM&T)

GM&T reported a total income of AED 175 million for Q1 2017 against AED 159 million for the same period in 2016. Non funded income saw a healthy growth y-o-y of 22 % mainly due to:

- GM&T Sales Desk revenue increase of 15 % year on year driven by higher volumes in Fixed Income sales & Foreign Exchange products

- GM&T Trading Desk delivering a good performance from Credit, Derivatives & FX Trading.

GM&T Global Funding Desk raised AED 3.3 billion of term funding through private placements.

Emirates Islamic (EI)

Emirates Islamic recorded a net profit of AED 221 million in Q1 2017, amidst challenging market conditions, a significant five-fold increase compared to the same period last year.

EI reported growth of 4% in total income (net of customers’ share of profit and distribution to Sukuk holders) amounting to AED 601 Million in Q1 2017 as compared to AED 579 Million in Q4 2016. The increase in total income is attributable to EI’s drive to continuously enhance the current product mix, improve margins and focus on non-funded streams of income. Operating cost continues to be tightly managed and the total cost has decreased by 18% compared to the same period last year. Net Impairment allowances have decreased by 60% compared to Q4 2016 due to effective remediation and an improved cost of risk associated with both corporate and retail financing receivables. During Q1 2017, Financing and Investing Receivables and Customer deposits remained flat at AED 36 billion and AED 41 billion respectively. EI’s focused approach to improve its liabilities mix and cost of borrowing led to a shift from expensive wakala deposits to incremental CASA balances. As at end of Q1 2017, CASA represented 69% of total customer deposits compared to 67% as at end of Q4 2016. EI’s Headline Financing to Deposit ratio at 87% remained comfortably within the management’s target range.

Outlook

We expect growth in the UAE to improve to 3.4% this year as higher oil prices contribute to improved consumer and business sentiment in 2017 and facilitate slightly higher government spending. We expect the UAE’s growth to accelerate to 4.1% in 2018, with Dubai expected to enjoy stronger non-oil activity growth on the back of increased investment in infrastructure. Anticipation of a 5% VAT to be introduced in early 2018 may boost spending in the second half of 2017, as consumers bring forward purchases that otherwise would be made in 2018.

Please click here to view the Financial Statements and Investor Presentation.

UAE

UAE