Emirates Islamic, one of the leading Islamic financial institutions in the region, today announced its full-year financial results for 2015, with the bank reporting strong growth for the fourth consecutive year.

Dubai, 18 January 2016

Financial Highlights

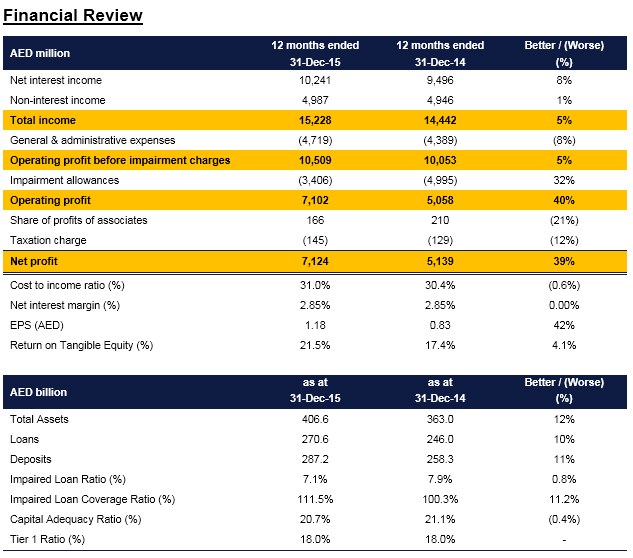

Emirates NBD (DFM: EmiratesNBD), the largest bank in the UAE by total income, net profit and branch network, delivered a solid set of financial results with net profit up 39% to AED 7.1 billion. The strong operating performance was helped by income growth, a modest increase in costs and a lower impairment charge. These results have enabled the Board of Directors to recommend an increase in the 2015 dividend to 40 fils from 35 fils per share.

Total income for the year grew by 5% to AED 15.2 billion. Net interest income grew 8% to AED 10.2 billion due to growth in assets and a lower cost of deposits. Non-interest income improved 1% to AED 5.0 billion as core fee income growth was offset by lower gains from the sale of properties and investments. Core fee income improved 14% y-o-y driven by growth in trade finance, foreign exchange and derivative income, alongside growing credit card volumes.

The Bank’s balance sheet remains strong due to further improvements in the credit quality and liquidity profile coupled with robust capital ratios. Despite a more challenging year for regional liquidity, the Bank’s Advances to Deposits ratio improved to 94.2% as a result of further growth in stable funding sources such as Current Account and Savings Account deposits. The Bank prudently issued AED 10.6 billion of term debt with most of this issued in the first half of 2015 when market conditions were receptive. The Impaired Loan ratio improved to 7.1% and the cost of risk declined for the sixth consecutive quarter whilst the Impaired Loan Coverage ratio increased to 111.5%.

Commenting on the Group’s performance, His Highness Sheikh Ahmed Bin Saeed Al Maktoum, Chairman, Emirates NBD said: “2015 marked another successful year for Emirates NBD as we continue to reach new milestones. I would like to take this occasion to congratulate His Highness Sheikh Mohammed Bin Rashid Al Maktoum, Vice President and Prime Minister of the UAE and Ruler of Dubai, on the 10th anniversary of his ascension as Ruler of Dubai. We are grateful for his vision, guidance and support that have greatly contributed to the success of Emirates NBD, Dubai and the UAE. During the year, and for the first time in the Bank’s history, total assets crossed the US$ 100 billion mark, total income exceeded AED 15 billion and net profit surpassed AED 7 billion, further reinforcing Emirates NBD’s position of leadership in the region. I am particularly pleased that Emirates NBD continued to achieve growth in revenue and net profit amid a challenging environment. As a leading bank in the region, we are well placed to take advantage of future growth opportunities in Dubai, the UAE and the Gulf region. In light of the strong performance by the Bank, we are proposing to increase the cash dividend to 40 fils per share.”

Mr. Hesham Abdulla Al Qassim, Vice Chairman, Emirates NBD said: “2015 saw a new phase for Emirates NBD as we continued to deliver improved profitability. Net profit increased by 39% to AED 7.1 billion helped by income growth, a control on expenses and a significant improvement in the cost of risk. During the year we continued to improve the Bank’s credit quality and liquidity profile. We have also completed the integration of the Egypt business onto Emirates NBD’s systems platform which will enable us to expand our presence. The Group is well positioned to continue to utilise our strong franchise and balance sheet to take advantage of growth opportunities in our preferred markets. We are confident that, going forward, our prudent business model shall continue to deliver a solid performance and deal with the opportunities and challenges that will present themselves.”

Group Chief Executive Officer, Shayne Nelson said: “I am pleased to report that Emirates NBD delivered a solid set of results in 2015. We delivered strong growth in net profit, supported by an enhanced asset mix, a further improvement in credit quality and an improved cost of risk. Our prudent balance sheet management and strong ability to attract and retain both retail and corporate deposits have enabled us to improve the Bank’s liquidity position despite a challenging year for regional liquidity. Costs remain firmly under control with a cost-to-income ratio of 31.0% for 2015, comfortably within our longer term target range. We continue to put the customer first with innovative products and excellent service. I am confident that Emirates NBD will continue to deliver excellent customer service and superior value to our shareholders.”

Total income for the year ended 31 December 2015 amounted to AED 15,228 million; an increase of 5% compared with AED 14,442 million in 2014.

Net interest income for the year improved by 8% to AED 10,241 million. The improvement in net interest income is attributable to an improved asset mix due to growth of Islamic and Retail assets and a lower cost of deposits helped by CASA growth.

Non-interest income grew 1% in 2015 to AED 4,987 million as core fee income growth was offset by lower gains from the sale of properties and investments. Core fee income improved 14% y-o-y due to higher income from trade finance, foreign exchange and derivatives, alongside growing credit card volumes.

Costs for the year ended 31 December 2015 amounted to AED 4,719 million, an increase of 8% over the previous year. This increase is attributed to higher staff costs linked with rising business volumes and partially offset by a control on other costs. The cost to income ratio increased marginally by 0.6% y-o-y to 31.0%. Excluding one-offs, the cost to income ratio is 32.7%.

During 2015, the Impaired Loan Ratio improved by 0.8% to 7.1%. The impairment charge of AED 3,406 million during the year was 32% lower than in 2014. The cost of risk has fallen for the sixth consecutive quarter as we see it trend to more normal levels. This net provision includes over AED 2 billion of write-backs and recoveries, and together helped boost the coverage ratio to 111.5%.

Net profit for the Group was AED 7,124 million in 2015, 39% above the profit posted in 2014. The increase in net profit was driven by income growth, a modest rise in expenses and reduced provisions.

Emirates Islamic, our key banking subsidiary, also delivered strong growth with Islamic Financing receivables growing by 24% during this period.

Loans increased by 10% and Deposits by 11% during 2015, and the Advances to Deposits Ratio improved to 94.2% from 95.2% at end 2014 due to the Bank’s strong structural liquidity supported by a stable retail CASA base. During 2015 the Bank prudently raised AED 10.6 billion of term-funding, which now represent 10% of total liabilities.

As at 31 December 2015, the Bank’s capital adequacy and Tier 1 capital ratios were steady at 20.7% and 18.0% respectively.

Business Performance

Retail Banking & Wealth Management (RBWM)

RBWM reported an operating income of AED 5,691 million in 2015, continuing its growth story in revenues, balance sheet and market share. Fee income accounted for AED 2,152 million, a strong growth of 12% over 2014 driven by an increase in foreign exchange remittance and the credit card business. Fee income now accounts for 38% of total income.

Despite the strong headwinds of continued weakening of oil prices, a strong dollar and slowing market conditions, RBWM has further improved its liability mix. Current And Savings Accounts (“CASA’) balances continued to grow in 2015, supported by a successful deposit mobilisation campaign, and now represent 84% of total deposits. The bank’s focus on sourcing higher value customers through the “Beyond” proposition is bearing fruit with new customer acquisition for mass-affluent segment growing by 34%. The bank’s DirectRemit instant remittance service has been extended to Sri Lanka in addition to India, Pakistan and the Philippines and has seen consumer remittance volumes grow fivefold.

The Retail Assets business saw healthy growth in loan volumes although loan margins saw some compression. Total advances grew 12% during 2015 to AED 34 billion. The Credit Cards business grew 21% helped by over 100,000 new card customers. The Bank launched several new co-branded cards, such as the Emirates NBD Starwood Preferred Guest credit card and the Emirates NBD DMCC corporate card, consolidating its position as the leading cards business in the UAE.

RBWM continues to lead the digital banking space and customer engagement & experience within the region. The Bank’s continuing investment in digitisation is resulting in increased migration of transactions and services to online and mobile platforms. The Bank’s mobile banking platform was enhanced with a full biometric log-in capability – Smart Touch and with a remote cheque deposit facility. Online and mobile banking transactions grew over 27% during the year, whilst branch transactions dropped by about 17%.

The Bank’s Private Banking business has shown strong growth in its core segments across the Gulf countries and the Global South Asian segment. Revenues grew year on year across different product lines and various geographies. Despite the market turmoil, Emirates NBD Asset Management successfully maintained its regional leadership position by growing Assets under Management to over AED 11 billion, largely driven by net inflows from local, regional and international institutional investors. Similarly, Emirates NBD Securities maintained its market share by widening its geographic coverage through the launch of a new mobile-based trading platform.

Wholesale Banking (WB)

Wholesale Banking, delivered a strong performance in 2015 with income up by 2% to AED 4,928 million compared with AED 4,816 million for the previous year ended 31 December 2014.

Net interest income in 2015 grew by 3% to AED 3,611 million compared with AED 3,510 million for the previous year, arising from a combination of asset growth and a reduction in non-performing loans.

Fee income for the year ended 2015 increased marginally by 1% to AED 1,317 million, compared with AED 1,306 million in 2014, reflecting continuing efforts to grow non-funded income with a strategic focus on increasing the Bank’s cash management and trade finance business along with the sale of Treasury solutions.

Costs were up by 14% compared with the previous year mainly due to inflationary pressures and selective initiatives undertaken to reshape the business. Wholesale Banking is continuing to invest in upgrading its Transaction Banking systems to improve levels of straight through processing and in Global Markets & Treasury (“GM&T”) where the system upgrades will support the Bank’s recent significant enhancement in GM&T product capability.

The credit quality of the loan book continued to remain strong, backed by the successful resolution of legacy portfolio issues which led to increased recoveries. This resulted in an improvement in the overall level of provision coverage and a fall in provisioning requirements by 48% to AED 1,983 million, compared with a provision of AED 3,797 million for the previous year ended 2014.

In terms of balance sheet, despite some market challenges, assets grew by 13% compared with the previous year with economic growth underpinning the continued momentum in the lending activity and the growth in the Bank’s Trade Finance business. Deposits also grew, rising by 16% due to an increased focus on building liquidity throughout the year.

Wholesale Banking is continuing to make good progress in its transformation programme aiming to become the leading Wholesale Bank in the Middle East and North Africa by providing a full range of Wholesale Banking products and solutions to the Bank’s customers across the Region.

Global Markets & Treasury (GM&T)

GM&T reported total income of AED 199 million for the year ending 31 December 2015.

Income declined by AED 636 million during this period on account of re-alignment of internal management reporting and due to a combination of a reduction in the size of the investment portfolio as well as the roll-off of some balance-sheet hedges.

Sales revenues grew 16% on the back of higher volumes in Interest Rate hedging products and Foreign Exchange Sales.

Global Funding issued AED 10.6 billion of term debt through a mix of public deals and private placements in eight currencies.

Emirates Islamic (EI)

EI delivered a strong performance in 2015 and achieved significant growth of 25% in total income (net of customers’ share of profit) amounting to AED 2,432 million compared to AED 1,949 million in 2014. Financing and investing receivables grew by 31% to AED 34 billion during 2015. EI expanded its branch network to 60 with the opening of four new Branches. In order to enhance customer banking experience EI also added sixteen new ATMS & SDMs, bringing the total number to 190.

Net Profit grew by 76% in 2015 to AED 641 million. EI succeeded in improving the NPL ratio to 8.8% from 10.2% last year, while maintaining the coverage ratio at 90%. Through its strong credit risk management and conservative provisioning policy, EI was able to absorb the effects of recent ongoing economic volatility.

The Bank’s success continued to be recognized across the industry and globally. As part of our efforts to create a strong brand identity for Emirates Islamic – both as a leader in Islamic banking and the community, EI sponsored a number of summits and community initiatives. During 2015, EI received a long term issuer Default Rating of ‘A+’ with a Stable Outlook from Fitch, the global rating agency.

Outlook

Emirates NBD estimates UAE economic growth at 4% in real terms in 2015, down from 4.6% in 2014. We expect growth to slow further to 3.8% this year as a more cautious fiscal stance, tighter liquidity conditions and a strong dollar will continue to pose headwinds to non-oil growth, particularly in the services sectors. However, oil output is expected to rise in line with official targets and this should help to boost headline GDP growth. The Bank will continue to implement its successful strategy built around five core building blocks which include delivering excellent customer experience, building a high performance organisation, driving core businesses, running an efficient organisation and diversifying sources of income.

UAE

UAE