Net profits up 27% to AED 5.0 billion on higher income and lower provisions

- Net profits up 27% to AED 5.0 billion on higher income and lower provisions

Dubai, 27 October 2015

Financial Highlights

Emirates NBD (DFM: EmiratesNBD), the largest bank in the UAE by Total Income, net profit and branch network, delivered a solid set of financial results with net profit up 27% to AED 5.0 billion. The strong operating performance was helped by an increase in net interest income, a modest increase in costs and a lower impairment charge.

Total Income for the first nine months grew by 2% to AED 11.2 billion. Net interest income grew 8% to AED 7.6 billion due to growth in Retail assets and a lower cost of funds. Non-interest income declined by 7% to AED 3.6 billion due to lower gains from the sale of properties and investments. However, core fee income improved 14% y-o-y driven by growth in foreign exchange and derivative income, growing credit card volumes and higher asset management fees.

The Bank’s balance sheet remains strong thanks to further improvements in credit quality, robust capital ratios and strong liquidity particularly during a challenging quarter for regional liquidity in the banking sector. The Advances to Deposits ratio remained within management’s target range of 90-100% thanks to further growth in stable funding sources such as Current Account and Savings Account deposits. The Bank prudently issued AED 9.5 billion of term debt with most of this issued in the first half of 2015 when market conditions were receptive. The Impaired Loan ratio improved to 7.1% and the cost of risk declined for the fifth consecutive quarter whilst the Impaired Loan Coverage ratio increased to 115.3%.

Commenting on the Group's performance, Mr. Hesham Abdulla Al Qassim, Vice Chairman, Emirates NBD said: “I am very pleased that Emirates NBD continues to deliver improved profitability whilst the strength of the brand and balance sheet has allowed the Bank to deal with increased regional challenges. In the first nine months of 2015 Emirates NBD achieved a 27% growth in net profit to AED 5.0 billion. We delivered another milestone with the integration of the Egypt business onto Emirates NBD’s systems platform. The Group is well positioned to continue to utilise our strong franchise and balance sheet to deal with challenges and take advantage of opportunities within the region.”

Group Chief Executive Officer, Shayne Nelson said: “I am delighted that we have delivered another solid set of financial results, with healthy levels of growth in both net interest income and profit. Our prudent balance sheet and strong ability to attract and retain both retail and corporate deposits has helped offer protection against increased challenges that the region has experienced. Equally pleasing is the further improvement in asset quality and the ability to maintain liquidity ratios within our target management range. Our strong balance sheet will allow us to take advantage of any growth opportunities in our preferred markets. We are confident that, going forward, our prudent business model shall continue to deliver a solid performance and deal with the opportunities and challenges that will present themselves.”

Group Chief Financial Officer, Surya Subramanian said: The operating performance for the first nine months of 2015 is solid, as demonstrated by the growth in both the net interest income and profit. We took advantage of favourable market conditions to prudently raise AED 9.5 billion of term-funding in the first nine months of 2015. This decision to ‘front load’ our term-funding requirements in the early part of 2015 is paying dividend even as we can comfortably meet maturing liabilities and wait for more favourable conditions to re-enter the capital markets.”

Financial Review

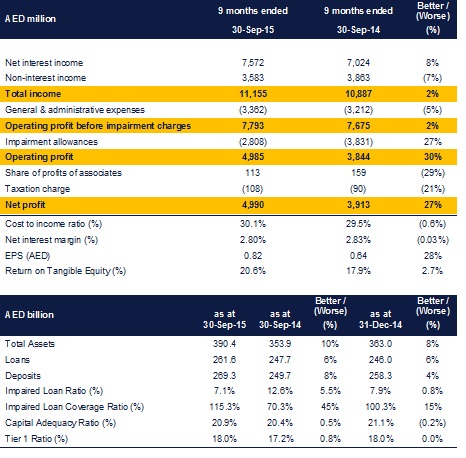

Total income for the nine months ended 30 September 2015 amounted to AED 11,155 million; an increase of 2% compared with AED 10,887 million during the same period in 2014.

Net interest income for the period improved by 8% to AED 7,572 million. The improvement in net interest income is attributable to an improved asset mix due to growth of Islamic and Retail assets and a lower cost of funds helped by CASA growth.

Non-interest income for the period declined by 7% to AED 3,583 million due to lower gains from the sale of properties and investments. However, core fee income improved 14% y-o-y due to higher income from trade finance, asset management, foreign exchange and derivatives.

Costs for the nine months ended 30 September 2015 amounted to AED 3,362 million, a modest increase of 5% over the previous year. This increase is attributed to higher staff costs linked with rising business volumes and partially offset by a control on other costs. The cost to income ratio increased marginally by 0.6% y-o-y to 30.1%. Excluding one-offs, the cost to income ratio is 31.7%.

During the first nine months of 2015, the Impaired Loan Ratio improved by 0.8% to 7.1%. The impairment charge of AED 2,808 million during this period is 27% lower than in the corresponding period of 2014. The cost of risk has fallen for the fifth consecutive quarter as we see it trend to more normal levels. These provisions, along with a healthy level of write-backs and recoveries, helped boost the coverage ratio to 115.3%.

Net profit for the Group was AED 4,990 million in the first nine months of 2015, 27% above the profit posted during the same period in 2014. The increase in net profit was driven by growth in net interest income, a modest rise in expenses and reduced provisions.

Loans increased by 6% and Deposits by 4% during the first nine months of 2015. Emirates Islamic also delivered strong growth with Islamic Financing receivables growing by 24% during this period.

Advances to Deposits Ratio increased to 97.2% from 95.2% at end 2014 as the market saw increased competition for deposits. During the first nine months of 2015 the Bank prudently raised AED 9.5 billion of term-funding. Term liabilities now represent 11% of total liabilities and help provide a strong cushion to deal with any future uncertainty in the global capital markets in the coming quarters.

As at 30 September 2015, the Bank’s capital adequacy ratio and Tier 1 capital ratios were steady at 20.9% and 18.0% respectively.

Business Performance

Retail Banking & Wealth Management (RBWM)

The division reported operating income of AED 4,265 million for the nine months ended 30 September 2015 reaching compared to AED 4,204 million over corresponding period in 2014.

Growth was primarily supported by a 14% increase in fee income driven by strong growth in foreign exchange and credit cards business. This helped improve the Fee Income ratio to 38% from 34% in 2014. Supported by the Current Account and Savings Account (‘CASA’) mobilisation campaign, the business grew its CASA balances by 5% in the first nine months of the year. Sourcing of mass affluent customers continued to rise month on month aided by the new “Beyond from Personal Banking” package.

The Retail Assets business continued to see margin pressure, though the growth in new volumes of Personal Loans and Auto Loans during the quarter has been healthy, aided by a number of successful campaigns. Total advances have grown 10% since the beginning of the year to AED 33.4 billion. The Credit Cards business achieved double digit growth whilst Debit Cards usage was maintained at the highest level of the market, consolidating the Bank’s position as the leading cards business in the UAE.

RBWM continues to lead the digital banking space. Mobile banking and online transactions have grown by over 30% this year whilst branch transactions have declined by 15%. Biometrics was introduced on mobile banking, for the first time in the region, with the launch of the Smart Touch feature. The flagship digital remittance service, DirectRemit, is now the dominant channel for individual remittances to the three corridors of India, Pakistan and Philippines. The product was further enhanced during this quarter with the launch of ‘DirectRemit to Mobile’.

Emirates NBD Private Banking also delivered growth thanks to an increase in revenue spread across different product lines and the various geographies. An increased focus on improving client service standards has resulted in increased customer satisfaction levels.

Wholesale Banking (WB)

Wholesale Banking delivered a steady performance for the period ended 30 September 2015 with operating income maintained at around the same level as the corresponding period ended 30 September 2014.

Net interest income for the nine months ended 30 September 2015 of AED 2,670 million was 4% lower compared with the same period in 2014, largely due to continued margin compression in a highly competitive market.

Fee income for the period ended 30 September 2015 increased by 6% to AED 1,017 million, reflecting a continued focus on the growth of non-funded income, with cash management, trade finance and the sale of Treasury products all performing strongly.

Costs increased by 14% for the first nine months of 2015 compared with the corresponding period in 2014 mainly due to investments undertaken to reshape the business, particularly in Transaction Banking, as the business seeks to improve its levels of Straight Through Processing

The credit quality of the loan book remained strong during Q3 while the successful resolution of legacy portfolio issues led to increased recoveries. This has resulted in an improvement in the overall coverage level and a fall in provisioning requirements.

In terms of balance sheet, assets grew by 6% during the year supported by good momentum in lending activity and growth in the Bank’s Trade Finance business. Deposits grew by 5%, as the business continued to build liquidity with a specific emphasis on Current Account and Savings Account balances.

Wholesale Banking continues to make good progress in its transformation programme aiming to become the leading Wholesale Bank in the Middle East and North Africa by providing a full range of Wholesale Banking products and solutions to the Bank’s customers across the Region.

Global Markets & Treasury (GMT)

GMT reported total income of AED 130 Million for the nine months ending 30 September 2015.

Income declined by AED 545 million during this period on account of re-alignment of internal management reporting and due to a combination of a reduction in the size of the investment portfolio as well as the roll-off of some balance-sheet hedges.

Sales revenues continues to grow on higher volumes in Interest Rate hedging products and Foreign Exchange Sales.

Global Funding issued AED 9.5 billion of term debt through a mix of public deals and private placements in eight currencies

Emirates Islamic (EI)

EI continued its impressive performance in the first nine months of 2015 with a 27% growth in total income (net of customers’ share of profit) to AED 1,801 million. Financing and investing receivables grew by 24% to AED 32 billion from AED 26 billion as of 31 December 2014.

EI aspires to become the leading Islamic Bank in the region and EI’s success is demonstrated by the 109% growth in Net Profit to AED 534 million for the nine months ending 30 September 2015. Islamic Financing continues to exhibit strong growth and EI has established itself as one of the three main Islamic Banks within the UAE. This success has been built upon an extensive branch network, a strong brand and a superior product offering.

EI recently received a long term Issuer Default Rating of ‘A+’ with a Stable Outlook from Fitch, the global rating agency, who also affirmed the bank’s support rating of ‘1’. This strong rating reflects EI's growing profitability, improving asset quality and high brand value. EI was also a high profile sponsor of the Global Islamic Economy Summit and is associated with a number of community initiatives.

Outlook

Emirates NBD recognises the headwinds that recent regional liquidity, a strong dollar and low oil price can present. The Bank is well placed to meet these challenges and to take advantage of opportunities within the region. As a result of the decline in oil prices and lower growth prospects for the global economy, the Bank last month adjusted its 2015 UAE growth forecast down to 4.0% (from 4.3% previously). We expect construction and manufacturing to remain important contributors to growth. Other non-oil sectors, including tourism, transport and logistics are also expected to grow. The Bank will continue to implement its successful strategy built around five core building blocks which include delivering excellent customer experience, building a high performance organisation, driving core businesses, running an efficient organisation and diversifying sources of income.

UAE

UAE