Dubai, United Arab Emirates, 28 January 2019: MENA fixed income instruments provided a relative oasis of calm against volatile market moves in 2018. MENA hard currency bond and Sukuk issuance reached USD 84 billion in 2018, with demand for new issues remaining high as regional debt was oversubscribed 2x -2.5x, according to a white paper by Emirates NBD Asset Management, KAMCO Investment Company and Fisch Asset Management. Investor appetite is likely to remain strong in 2019, as GCC bonds are included in the JP Morgan EMBI index series and regional governments sustain ambitious reform agendas. The co-authored paper, “MENA debt: an evolving world for fixed income investors”, provides an in-depth look at regional fixed income in 2018 and provides an outlook for 2019.

Financial markets in the MENA region are evolving at a fast pace and more outward-looking policies aimed at integration with global markets are increasing the breadth of financial instruments traded in the region, giving international and local investors compelling reasons for exposure. The case for fixed income portfolio allocation to MENA is supported by the growing share of global GDP represented by the region, which for the GCC is expected to increase from 1.8% in 2015 to 2.0% in 2019, while its share of emerging markets GDP is expected to increase from 4.7% to 5.0%.

Faisal Hasan CFA, CBDO & Head of Investment Research at KAMCO Investment Company, commented:

“Regional gross government debt as a percentage of GDP increased from 29.7% in 2014 to 44.4% in 2018, after a series of issuances. Fiscal deficits for most MENA countries have been the reason for an increase in government debt, and this trend is expected to continue in 2019 – providing a fresh set of opportunities for investors. Reforms being implemented across MENA make it an attractive destination for global investors - spending on infrastructure remains a priority for policymakers and expanding the non-oil sector to diversify economies away from oil dependence has received support from almost all governments in the region.”

Less than a month into 2019 the GCC has already delivered USD 9.1 billon in issuance from both sovereigns and corporates, including the Saudi sovereign, First Abu Dhabi Bank (Sukuk) and Dubai Islamic Bank (AT1), setting the scene for the rest of the year. In addition, there are market-wide expectations that Saudi Aramco will issue debt in 2Q19 to fund its SABIC stake acquisition.

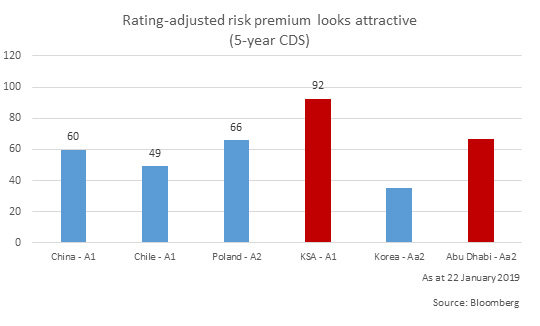

The paper also highlights that, while regional bonds look attractive on a ratings-adjusted basis against other emerging markets, there are a range of important considerations for investors: these include geopolitical uncertainty; possible rating downgrades, although in the case of most sovereigns this is mitigated by diversification initiatives; increased supply carrying the risk of a glut outstripping demand; and the region’s over-reliance on oil as a revenue source.

Parth Kikani CFA, Director Fixed Income at Emirates NBD Asset Management, said:

“Last year, GCC fixed income provided a safe haven during a sustained EM sell-off period. For 2019, we think risks are more balanced, and investors will need to be more discerning in credit selection. While risks stem from further oil price volatility, increased issuance and geopolitical uncertainty, investors may benefit from attractive risk premiums, improving fundamentals and the benefits of index inclusion leading to efficient price discovery. Moreover, with most GCC currencies pegged to the US dollar, this reiterates an attractive relative risk premium amid weakening emerging market FX rates and a stronger US dollar.”

Furthermore, financial sector subordinated papers are especially attractive for investors. These offer relative value as they benefit from unique features including no hard capital ratio triggers, substantial ownership stakes from GCC sovereigns, the absence of a taxpayer base that reduces moral hazard in the event of any pre-emptive capital injections and typically high distributable profits that protect against coupon skips. Given easy access to capital markets, issuers typically call issues on the first call date, so extension risk is heavily discounted, offering relative value to investors.

Philipp Good, CEO and Head of Portfolio Management at Fisch Asset Management, concluded:

“An important driver for investors, whose demand encourages new supply, has been a widening of spreads as a consequence of rising interest rates in the US. Until a new equilibrium in the rate market is found, emerging markets remain attractive alternatives for allocation, with GCC countries among the most appealing of all. Most countries are pushing their reform agendas, and the balancing of the pace of reform will be one of the key drivers for stability in the region. Meanwhile, oil price performance remains crucial, and a key driver for credit.”

Default risk in the GCC remains low despite volatility in oil prices. The GCC region has seen very few defaults or restructurings compared to broader emerging markets. Large government reserves - in the form of Sovereign Wealth Funds (SWFs) - offer support in times of distress and provide a liquidity cushion that can reduce default risk, which is considered a key differentiator from emerging market peers.